By clicking the “I Accept” button, or by accessing, participating, or submitting any information, or using the Jabil Global Intelligence Portal or any of its associated software, you warrant that you are duly authorized to accept the Global Intelligence Portal Terms and Conditions on behalf of your Company, intending to be legally bound hereby, and your company shall be bound by the terms and provisions of the Global Intelligence Portal Terms and Conditions, accessible under the following link Portal T&Cs.

Jabil's Global Category Intelligence Archive

Global Category Intelligence

Q3 2023

Jabil's Global Category Intelligence Archive

Global Category Intelligence

Q3 2023

PROFESSIONAL SERVICES, CONTINGENT LABOR

AMERICAS

Market Overview

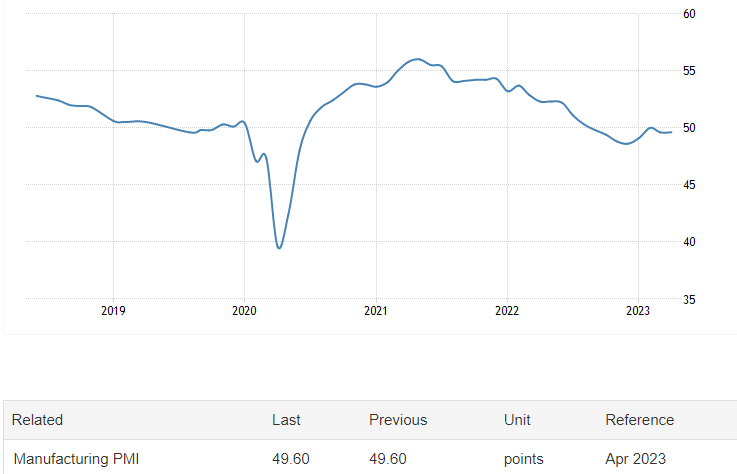

- According to JPMorgan’s Global Manufacturing Purchasing Managers’ Index, the overall global PMI has been below 50 since September 2022, ending at 49.60 in April 2023. While below 50, it is on par with September 2022 and is a little below February 2023, which briefly closed near 50. The overall index remains at its lowest level since 2020.

- Overall global economic expansion was noted in Q2 2023, however largely led by services PMI that was over the baseline of 50 at about 52.8, while manufacturing remains in contraction territory.

- The large gap in services was due in large part to the full opening of China, post-COVID-19 restrictions, meaning people were free to move about as containment measures subsided. Overall manufacturing output rose for a third straight month but is still in contraction.

- Improved supply chains are contributing to the improvement in output efficiency.

- The potential for recession and softening of demand may dampen the inflation rate somewhat, but employers can expect the challenges around attracting and retaining quality labor resources to continue.

- Competition for contingent labor and flexibility will continue to drive demand forecast uncertainty, but large consumers of staff augmentation will benefit from the flexibility a temporary labor force provides during swings in demand.

Demand Commentary

United States

- The April 2023 PMI ended at 46.3, down from 47.7 in March, as the US saw its manufacturing activity slow to a three-year low. New orders plunged, in part due to multiple interest rate increases that were aimed at curbing record inflation.

- The US Bureau of Labor Statistics core inflation rate (excluding food and energy) eased to 5.5—only one basis point from March’s 5.6 but in line with Fed forecasts.

- The US unemployment rate ended at 3.4% in April, matching January’s record low and the lowest level since 1969.

- Manufacturing added 11,000 jobs in April after shedding 8,000 in March.

- Unemployment in manufacturing is at 2.8 percent.

- The US Bureau of Labor Statistics core inflation rate (excluding food and energy) eased to 5.5—only one basis point from March’s 5.6 but in line with Fed forecasts.

Canada

- Canada’s manufacturing PMI climbed back over the expansion line of 50 to 50.2 in April 2023, reversing its decline from March at 48.6 which was a three-year low, but lower than February’s 52.2. The increase was tied to higher output from higher staffing levels in factories. There is a continued drop in new orders, meaning the increase may primarily be due to clearing backlogs.

- The longer-term PMI is forecast to trend to around 55 in 2024, even while general business confidence moves to a positive but more conservative outlook.

- The overall unemployment rate remained at 5.0% in April for a fifth straight month.

Brazil

- Brazil’s PMI fell to 44.3 in April 2023, down from 47 in March. This marks the sixth month in a row of contraction in factory activity. Production fell to its lowest level in three years.

- Additional declines in new orders resulted in job losses while prices have increased.

- Compared to other Latin American countries, Brazil’s economic growth is expected to be one of the weakest in 2023, ahead of only Argentina. Negative sentiment is increasing as lower interest rates have not supported growth, resulting in the lowest confidence in 18 months.

Supply Commentary

United States

- Manufacturing job openings have decreased to 693,000 in March, about 200,000 lower than a year prior; Many companies are eliminating previously open positions.

- Manufacturing companies are also cutting back on current jobs. Between February and March 2023, there were 415,000 separations while hires fell to 393,000 over the same period. This is the first time since April 2021 that there were more separations than hires in manufacturing, according to BLS archives.

- Temporary help fell by 23,300 jobs in April, reversing growth of 26,000 in February.

- Temp agency penetration rate fell to 1.93% in April, a measure of the percent of total nonfarm employment.

- The prospect of a recession in the US has companies pulling back on the use of temporary and contract workers.

Canada

- There are approximately 3.9 million ‘industrial workers’ in Canada which includes manufacturing, construction, and natural resource extraction.

- The number of jobs in this sector has not grown in five years, however, it has not shrunk either. 1.7 million (44%) of these jobs are in manufacturing.

- One-fifth of these manufacturing workers are over 55 years old, while 22% are under 24; this may create issues soon if more is not done to attract younger workers as older ones exit the labor force.

- Companies continue to struggle to find enough workers, with many still turning to the TFW (“Temporary Foreign Worker” Program) for help.

- The labor market is so tight that the Government is introducing a two-year measure that will allow family members of current foreign national workers to apply for their work permits in 2023.

- This program used to only be for those in high-skilled roles but is being opened to lower-stream wage roles as well.

Brazil

- Brazil’s unemployment rate rose to 8.8 percent in March, up from 7.9 percent in December, but still lower than the forecast of 9 percent.

- Overall, Brazil’s labor force participation rate hit 61.60 percent in March 2023, down from an all-time high in September 2022.

- Experts expect this to remain relatively consistent into 2023 and coupled with low unemployment figures, the availability of labor, including flex/temporary labor, remains tight.

- Temporary worker labor laws in Brazil, similar to Mexican labor laws, have regarded temporary labor that is deemed to be core to a company’s main line of business as not approved, while ancillary roles are approved.

- However, in August 2018, outsourcing roles that are core to a company’s core business became legal. The typical temporary employment agreement is for a 180-day duration and can be extended further by 90 days.

- Most temporary workers are brought in to replace a full-time employee, for example, one who may be on a leave of absence.

Pricing Situation

United States

- In April 2023, real wages for production and non-farm/non-supervisory employees grew 4.95% year over year. The average hourly earning for non-farm payroll was $28.62 in April 2023.

- Durable Goods Manufacturing jobs averaged $27.25 per hour in April 2023, up from $26.07 in April 2022, or 4.52% Y/Y.

- Canada- Average hourly wages in manufacturing were $22 CDN (about $43,000 CDN per year) in early 2023.

- More experienced workers can make over $120,338 CDN per year; Operators average $39,000 CDN, and Installers average $48,750.

- Overall average minimum wages are expected to reach around $16.50 CDN in 2023.

Brazil

- The average salary of a person working in a factory in Brazil in 2023 is approximately 5,850 BRL per month (USD 1,168), including housing, transport, and other benefits. According to salaryexplorer.com the monthly pay range for factory and manufacturing roles is between 3,820 BRL and 14,700 BRL depending on tenure and role (USD 763 to USD 2,936).

- In April 2023, the average wage, not inclusive of benefits, housing, and transport, was 2,741 BRL (USD 547) up 7.1 percent year over year.

- On May 1, 2023, minimum wage increased to 1,320 BRL (USD 264) per month, a 4.1 percent increase from January 2023.

APAC

Market Overview

- In Q2 2023 most Asian manufacturing demand faced continued softness, however, recent confidence and growth in output and new orders within India provide some optimism for the region.

- The largest economies in Asia are still hovering a little below 50 on their respective Manufacturing PMI ratings, signaling cautiousness among larger manufacturing firms. There is a shift for some companies to move production from China, with India being the primary focus for building alternative capabilities.

- A year ago, as global demand began to climb, factories were committing to use more monthly-based outsourced workers.

- This trend is now shifting towards more hourly-based arrangements to better accommodate flexibility in total hours worked and balance fluctuations in customer demand schedules.

- Availability of contingent labor in Asia markets has continued to ease in Q2 2023, continuing a trend toward additional availability post-Chinese New Year and due to production pullbacks as overall demand and new orders continue to fall.

- Q2 2023 has also seen a global ‘explosion’ in interest around artificial intelligence (AI) and machine learning (ML), with manufacturers, engineers, and the world’s biggest hard goods providers launching use cases for applying AI and ML on the factory floors.

- Many of the advancements are likely to change the future demand for laborers.

Demand Commentary

China

- China- China’s NBS Manufacturing PMI ended at 49.5 in April 2023, continuing the roller coaster ride so far since the start of the year but in slight contraction mode.

- Overall requirements for direct labor have been declining in line with the reduction in output growth. Delivery orders have improved given the slower overall production.

- Demand for lower-skilled labor has slowed (at the same time).

- Demand for qualified technicians continues to increase.

Malaysia

- Malaysia’s manufacturing PMI ended at 48.8 in April 2023, up from 46.5 in January 2023, but still the eighth straight month of contraction, below 50.

- Global demand for Malaysian manufactured goods remains subdued.

- Confidence in the current economic outlook fell to a four-month low as well. Despite the gloomy outlook, manufacturers are hopeful that global demand will start to recover and move them into expansion territory by summertime or the start of Q4, with the PMI projected to hover around 50.

- Net trade contributed negatively to GDP with exports falling by 3.3% and imports dropping by 6.5%

- Manufacturing as a % of total GDP continues to fall in Q2 2023, falling by about 5.7% from the end of Q1 2023.

Singapore

- Manufacturing PMI remained at 49.7 in April 2023, the eighth straight month of contraction and falling slightly from February amid softness in the electronics manufacturing sector, which now comprises about 42% of industrial output, rising 2% since January.

- Economists expect a further erosion of output into the second half of 2023 with recovery estimates uncertain in the near term.

- Demand for labor has become even more restricted as the unemployment rate fell to 1.8% in Q1 of 2023, the lowest jobless rate since early 2015.

- There were about 4,000 persons laid off during Q1 retrenchment, led by jobs in manufacturing and construction.

India

- India’s Manufacturing PMI ended April at 57.2, up from 56.4 in March and close to January’s 57.5 as new orders continued along with improved delivery times. India remains a bright spot in global manufacturing and growth is expected to continue, but perhaps at a slower rate into the remainder of 2023 as input cost inflation has accelerated.

- While forecasts show continued growth, India’s GDP is widely expected to average 6.4% in 2023, up from earlier estimates of around 4%. Asian Development Bank expects the GDP to rise to 6.5% by the end of India’s fiscal year end on March 31, 2024.

- In recent months, renewed interest in substantially growing India’s global manufacturing footprint has occurred. Several large global electronics companies have started to look beyond China in response to uncertainty around covid lockdowns and the risk they pose to production and supply chains. Currently, manufacturing’s contribution to India’s economy is under 15%, compared to a bit over 25% in China.

- India’s Ministry of Electronics and Information Technology put forth a ‘vision’ earlier in 2022 to transform the country into a $300 billion powerhouse by 2026, up from $75 billion in 2021.

Vietnam

- Vietnam’s Manufacturing PMI continues to see-saw, ending at 46.7 in April 2023, but that was the fifth measure below 50 in the last six months and the lowest result since December 2022.

- Manufacturing production continues to decrease and as a result firms are reducing staffing levels, both via attrition and retrenchment.

- Several recent free-trade agreements with the European Union, and United Kingdom, and a Trans-Pacific Partnership have further strengthened the manufacturing position and attractiveness of Vietnam.

- With these partnerships, Vietnam should be in a good position to support growth in demand with the expected PMI to be 53 in 2024 and 52 in 2025, indicating expansion.

Supply Commentary

China

- In Q2 2023, given economic slowdowns, reduced demand overseas, and a return to more normal market conditions, there is currently an ample supply of contingent labor to meet requirements.

- This is the first time in about three years that supply has stabilized against current demands. However, when the Manufacturing PMI heads above 50 again, the supply may be tight as some workers leave for better-paying jobs, including those recent college graduates who have been taking manufacturing direct labor roles as their initial employment out of school.

- According to the International Monetary Fund, reforms will be required in the short term for China to deal with a declining work population.

- Ideas, such as raising the retirement age, increasing health insurance benefits, and closing productivity gaps for state-owned enterprises may help. The goal is to raise China’s overall income levels by 2.5% to increase demand and boost the economy.

- China’s growth in working-age population allowed it to grow exponentially over the last several decades, but projections by the United Nations Department of Economic and Social Affairs have China losing about half its population by the end of the current century if today’s low birth rates continue.

- There is an evolution happening around the skill sets required for blue-collar jobs given the move toward more automation and intelligent manufacturing. The expectation for more technical workers within this demographic is to be able to work more technical equipment and other digital technology.

- Manufacturing comprises about 18% of China’s labor force, with the majority having only a middle-school level education.

- As a result, and due to the current economic downturn, economists recommend that training be a major focus for large-scale factories, with government support for those classes.

- At risk is China’s future ability to attract and retain some of the world’s largest brands, which have eyes on India, Vietnam, and abroad in terms of moving production.

- India is expected to surpass China during 2023 to become the world’s most populous country; More importantly, in a few more years India will surpass China’s working population age, defined as people 20-69 years old.

Malaysia

- About 30% of Malaysia’s workforce is comprised of foreign workers with about 7.25 million persons compared to 16.5 million Malaysian citizens.

- Unemployment fell to 3.5% in March 2023, down from 4.1% year over year.

- The labor force participation rate remained at 69.90% in March 2023, unchanged month over month, indicating steady employment, even with reduced demand for manufacturing contingent labor.

- Recruiting foreign workers remains a key element of continuing and ensuring the growth around electronics manufacturing, however, some companies have put a hold on bringing in additional foreign workers during the downturn in demand.

- Typically, quotas issued by the government to recruit foreign workers are good for up to two years, so firms may find themselves having to request new allocation approvals from the government if they do not use their full allocation, depending on the timing of any recovery and output increase.

- Companies that utilize foreign worker schemes have put more focus on vetting the RBA compliance of the agencies, and in particular their in-country agents who recruit new workers.

- Increasing reliance on foreign workers can bring risks around compliance if the full supply chain is not fully investigated, rather than just on the receiving supplier.

Singapore

- Total employment grew by 34,500 in Q1 2023, up for the sixth straight quarter, however, the growth is slowing.

- Singapore leaders continue to want to attract higher skill level foreign workers, however, they still offer work pass applications under the “Work Permit for Migrant Worker” program for manufacturing and other similar sectors.

- The program is like those in other regional countries such as Malaysia, however, there is no minimum stipulated salary, but there is mandatory insurance coverage, semi-annual health checks, provide housing, and pay a monthly levy.

- The Ministry of Manpower plans to lower the quota of foreign workers in the manufacturing sector from 20% of the workforce to 15%, beginning in 2023, to focus on higher-skilled roles and industries being attracted to Singapore.

- Companies largely still focus on hiring direct labor given the shortage of S-Pass rules around foreign worker investment and regulations.

India

- India’s relatively strong economic outlook bodes well for employment for a younger generation as private investment in new manufacturing capacity will open new opportunities, even while the rest of the world contracts a bit.

- In the near-term India is facing difficult headwinds around the current and future supply of workers, as according to the CMIE (Centre for Monitoring Indian Economy), in 2021 57% of the overall workforce is in their forties and fifties, and only 40% of working-age citizens are employed. While unemployment has stabilized, the industry is not creating enough quality or decent-paying jobs. Only 20% of jobs are ‘formal’ meaning regular wages and job security.

- The educational qualification has been declining as well in recent years, with 12.2% of the population being graduates or post-graduates, down from 13.4% in 2018.

Vietnam

- In January 2020, Vietnam had a workforce totaling about 56 million. In March 2023, that number had fallen to 51 million. In mid-2022 the labor participation rate was 76% but has fallen to 68.9% in March 2023. However, only about 12% are considered highly skilled, and only about 26% are trained at all.

- In order to raise the vocational acumen of the labor force, the government enacted “Decision 17” in mid-2021, aimed at offering free vocational training to unemployed workers who meet certain criteria. There are options for 3 months and extended training based on the type of support and a cap on reimbursement.

- In June 2021, the Government of Vietnam issued “Decree 57” which offers corporate tax incentives (CIT Incentives) which give full exemptions for four years, a 50% reduction for nine years, and a 10% preferential tax rate on the first 15 years on income coming from the project.

- Electronics manufacturing is one of those industries that can use the incentives.

Pricing Situation

China

- Real wage increases for 2023 should average about 3.8%.

- Requirements are shifting back to hourly rates, not monthly “outsourcing” needs to allow flexibility to reduce the workforce when the demand has been met, rather than taking on a full month of pay.

- Hourly rates for direct labor manufacturing roles have dropped compared to a year ago in cities like Shanghai, Wuxi, Guangzhou, and Shenzen, in accordance with local city law requirements, but as business operational demand has weakened, as well.

- Annual salaries for ‘general’ blue-collar workers are projected to be 80,000 RMB ($11,500 USD) on the low-end, to 120,000-150,000 RMB for higher-skilled jobs ($17,000-$21,000 USD).

- Regional governments are required to raise minimum wages at least every couple of years. The average overall hourly wage ranges between 14.9 Yuan (Anhui province) and 25.3 Yuan in Beijing and Shanghai.

- Specific to migrant workers in electronics manufacturing, skilled labor can pay up to about 8,000 RMB per month ($1,120 USD), whereas those lacking experience on a production line may earn between 3,500 to 5,500 RMB ($500-$775 USD) per month.

Malaysia

- The minimum wage increased to 1500 MYR per month in May of 2022, however, they have not increased in a year, as of May 2023. Companies with less than five staff members are also now going to increase their minimum monthly salary to 1500 MYR as of 1 July 2023.

- Economists had been predicting a wide range in terms of potential wage increases during 2023, between 3 and 20%, however, most should average about 5.1%, with the higher increases reserved for higher niche skills and IT-related industry workers.

- It remains to be seen what effect the decrease in maximum weekly hours worked from 48 to 45 may have on the need for shift work to hire additional resources to cover the reduction but depending upon the number of foreign workers a company needs; it may be significant. In addition to hourly wages, extra expenses would be recognized around recruiting, travel, training, housing, food, and wellness. Overall hours worked are increasing in 2023 to above 30 hours per week as the country fully emerges and recovers from covid-era pullbacks in hours worked.

- Total salaries and wages paid in manufacturing increased 5.4% year over year to 7.9 billion MYR ($1.7 billion USD) in September 2022.

Singapore

- According to Employment Conditions Abroad (ECA), the average worker in Singapore will see a 3.8% increase in base salary. However, given current inflation rates, their real wages decreased by about 1.7% in 2022. Accounting for currently expected inflation rates, the expected net real-salary increase in 2023 is 1.0%.

- The average hourly wage across all industries in Singapore is 33 SGD ($23.53), or about 5676 SGD $4,000 USD per month ($23.53 USD). Within the Manufacturing and Factory sector, the average monthly salary ranges between 2,140 SGD and 14,500 SGD (between $1525 and $10,337 USD) per month, from entry-level to leadership.

- According to industry surveys conducted in May 2023, the average salary for a contract worker in Manufacturing & Labor Worker sectors is 85,430 SGD per year, a 1.0% increase from February 2023.

- The salary increases, on average, about 9% every 15 months in manufacturing.

India

- The minimum wage of 178 INR per day ($2.23 USD) has not increased since 2018, however, the forecasted “India National Floor Level Minimum Wage” is expected to hit 185 INR per day in 2023, and 190 INR per day in 2024.

- There is no country-level minimum wage requirement, but it can be set by the state or even the industry sector.

- The average wage of a manufacturing worker per month is 21,800 INR ($273 USD), with a low of 8080 INR ($101 USD) to a high of 54,600 INR ($685 USD). This is about 32% lower than other jobs in India.

- The average hourly wage of a factory worker is 130 INR ($1.63 USD)

- Recent pricing proposals for the management of contingent work in India have seen monthly management fees averaging about 800 INR per head per month ($9.68 USD), with a range of 500 INR to 1,194 INR ($6.05 USD to $14.45 USD).

Vietnam

- Vietnam remains an attractive country for manufacturing when compared to China and other countries in Asia.

- The average monthly wage for a manufacturing role in Vietnam is US $336 (7,900,000 VND) in March 2023, up 3.9% from Q4 2022.

- For comparison, China’s monthly wage is about $1,150 USD (26,993,375). Low-skilled/entry level is about $229 USD per month (5,375,202 VND).

- Despite the lower cost, Vietnam has 14 times fewer workers than China.

- Depending on the region, the minimum wage increased on July 1, 2022, by about 6% overall.

- The government was moved to act based on the large price hikes around fuel, the Russia-Ukraine conflict, and general inflation.

EUROPE

Market Overview

- In April 2023, the International Monetary Fund’s World Economic Outlook forecasted euro area aggregated GDP for 2021 at 0.8%, which is an increase from the January outlook of 0.7% and 0.3% higher than originally predicted in October 2022.

- The UK’s outlook improved slightly from January but is still forecasting negative growth, while Germany’s fell below zero, predicting a -0.1% GDP in 2023.

- The IMF was initially predicting that the world’s economy would have a ‘soft landing’ with forecasted slower inflation, however, record rises in interest rates have created banking challenges, leading to a more pessimistic view that chances of a ‘hard landing’ have increased.

- According to a Eurofound, 2023 is “Europe’s year of resilience and resolve.” Despite flat GDP growth, there is still optimism.

- The Great Resignation that swept the world in 2022 has given way more to a Great Reassessment whereby workers are not just leaving jobs, but moving to jobs offering greater flexibility, and work-life balance and as a result have kept unemployment levels low.

- People are still adapting to high inflation resulting in large part from the conflict in Ukraine. Growth in sustainability industries and the digital economy kept employment options and levels at overall positive levels.

- Euro area 2024 GDP is projected to grow to 1.4%, down from 1.6% as predicted in January 2023. with the effects of efforts to stifle inflation expected to improve in areas like energy and food prices.

- Below are some key labor market dynamics, supply trends, and pricing impacts in select European countries; much of the feedback applies across the entirety of the euro area.

Demand Commentary

Switzerland

- In April 2023, the manufacturing PMI index fell further to 45.3, the fourth consecutive monthly decline and down from 54.1 in just December 2022. New order declines and significant backlog reductions continued. Some analysts still predict PMI to hover around 50 by the end of Q3, while others are more conservative.

- The brighter news is that the inflation rate dropped to 2.6% in April, its lowest rate in 12 months. Prices slowed as prices stabilized for things like housing and energy.

- It remains slightly higher than the average historical rate of 1.5-2%. Experts forecast rates to return to historical averages in 2024 and 2025.

- One major change related to economic uncertainty has been a shift away from demand for temporary labor and more in favor of permanent positions.

- Demand for temporary labor declined by 3.4% in April 2023, the first such fall in over two years at the height of the pandemic.

- Softening demand in manufacturing has reduced the need for temporary workers. More companies are hiring permanent staff, either by converting temp-to-perm or direct hire, resulting in more demand stability and better retention rates.

- A few industries, such as healthcare, have seen steadier demand, but not yet an increase in 2023.

Germany

- Germany’s manufacturing PMI ended at 44.5 in April 2023, continuing a ten-month trend of contraction, and the lowest since May 2020. Downward pressure on new orders is sustaining the pessimism. Inflation rates continue to fall, trending toward 7.2% in May 2023, down 1.5% since February 2023.

- With expected flat to negative GDP growth in 2023, economists predict a 5% decline in temporary employment activities during the year.

Hungary

- After starting 2023 with PMI hovering around 55, it increased to 61.9 in April 2023. According to HALPIM (Hungarian Logistics Procurement and Inventory Management), foreign market indicators continue to show growth while finished goods inventories increased as well by 7.8% indicating expansion and tempered optimism.

- Inflation eased a bit in April 2023, ending at 24% as prices slowed for consumer basics and utilities. However, the rate is still not far off from the 27-year high of 25.6%, but less than market forecasts.

Ukraine

- Although the combat to date in Ukraine during the Russian invasion is highly localized to the eastern side of the country, the overall GDP in 2023 is projected to be only 0.5%. According to the World Bank, since the start of the war poverty has increased from 5.5% to 24.2% of the population, resulting in another 7.1 million people being pushed into poverty.

- Exports remain low due to a lack of infrastructure and disrupted supply chain routes.

- Prior to the war, manufacturing accounted for 11.7% of Ukrainian GDP, with plans to have about $2 billion USD in foreign investments in manufacturing within Ukraine.

- Ukraine’s robust IT Staff Augmentation industry has adapted during the crisis, either by re-deploying resources into Western Europe or relocating their resources to other hot spots, such as Latin America, which has been the case for many larger firms.

- It should be noted that operations sited within Western Ukraine are continuing to service most clients well as the war's combat activities have so far had a lesser impact upon that region of the country.

Supply Commentary

Switzerland

- Labor shortages are still acute across Switzerland, despite the economic cooldown.

- While the increase in working hours across the temporary market has flattened in 2023, demand for permanent workers has risen dramatically in 2023 over 2022.

- Less than half of staffing providers think there will be an increase in temporary worker demand.

- Workers in specialty industries or positions have increased their leverage for wage bargaining power, and companies are doing all they can to retain them as long as possible.

Germany

- Lower economic growth has companies pulling back on hiring; while declining market volumes will also lead to lower demand.

- Germany is already a market that doesn’t use a lot of temp labor (about 1.7% of the workforce on average, compared to about 3% for France, the UK, and the Netherlands) so a slowdown in demand won’t necessarily open up a lot of available temp labor supply.

- Among the age range 15-29 (of those not participating in formal education), about 17% work via temporary contracts.

- Unemployment has held relatively steady at 5.6% since the summer of 2022.

Hungary

- Hungary’s unemployment rate hovered around 4.1% in March/April 2023, a slight increase from 3.8% the prior quarter. It has been slowly increasing over the last year, from a 12-month low of 3.5%.

- Industrial production declined 4.1% in March across most of the manufacturing sub-sectors, except for heavy vehicles and electrical equipment. Electronic and computer production, which accounts for 9% of total production, fell 13.8% year over year in March 2023.

- There remains a shortage of skilled workers, further challenged due to an aging population.

Ukraine

- The International Labor Organization estimates that about 5 million people have lost their jobs or been displaced from work because of the war. This translates to an unemployment rate of 35% or triple the average before the invasion.

- According to the National Bank of Ukraine, unemployment is estimated to be about 20% in April 2023, with the recovery of employment slowing in Q1 2023 despite some improvements in the labor market. There are regional disparities because of the war, and the number will struggle to fall as migrants start to return from abroad.

- As reported by Work.ua (Ukraine's largest job search site) in western regions like Lviv, the number of job openings has returned to about 80% of pre-war figures, although primarily within the hospitality sector.

- In May 2023, there were 2,250 vacancies listed for manufacturing roles, including production workers, milling debuggers, production operators, and management-level production jobs.

Pricing Situation

Switzerland

- The average annual salary of a factory worker in Switzerland is currently about 49k CHF (about $52k USD), which equates to about 24 CHF per hour ($25.50 USD). This is for roles such as line worker, assembly foreman, dock worker, and equipment operator.

- The current minimum wage is also 24 CHF per hour (as of April 2023) and is subject to adjustment annually based on the consumer price index.

- Long-term projections anticipate an 11% increase over 5 years to 54k CHF by 2028 or a non-compounded annual increase of just over 2%.

Germany

- According to salaryexpert.com, the 2023 average annual base wage in manufacturing in Germany is 33.06 EUR ($34,800 USD) for roles as machinists, assembly line workers, demand planners, and factory workers.

- The average range for factory salaries is between 27k EUR (1-3 years of experience) and 39,281 EUR (8+ years of experience)

- The average wage increases in 2023 is expected to be about 2.5%, however, with the cost of living increasing by 8.3%, real wages are declining.

- In early 2023 trade unions representing temporary workers negotiated increases for about 816,000 workers in specific pay groups from April 2023 and in January 2024. The pay increases will amount to about 13.07% for pay groups 3 and 4, and about 9% for wage group 9.

Hungary

- Hungary’s gross average wages rose 0.8% year over year in February 2023, leading to the smallest year-over-year monthly gain since 2014. However, the 16% adjustment in January 2023 to help offset eroding real wages due to inflation is not a sustainable month-over-month comparison.

- The average monthly salary was 531,200 HUF in February 2023.

- Real earnings in February fell 19.6% when factoring in inflation. Note, that when excluding the ‘service premium’ portion of this for military and police six-month salary, (which amounts to 11.8% of this amount,) the net decrease was 7.6%.

- The average monthly salary for a factory worker in Hungary is 337,000 HUF (821 EUR/$819 USD), which is about 45% above the current overall minimum average wage of 232,000 HUF that was implemented in January 2023.

Ukraine

- With inflation in the double digits and no timeline for a resolution to the conflict with Russia, those companies with other global service centers are offering options ranging from a low of 11% to over 20% hourly rate increases for resources in Application Development, Systems Analysts, and Data Architects. Price increase requests for those remaining in the country have ranged from 10-20% in recent months.

- Average annual wage growth entering 2022 was about 18%, with estimates for Q1 and Q2 of 2023 hovering around 8%.

- As of May 2023, the national minimum wage is UAH 40.46 per hour/ UAH 6,700.00 per month, on a maximum 40-hour work week. ($1.10 USD per hour/$181.39 USD per month).

Back to Top